Image 1 of 3

Image 1 of 3

Image 2 of 3

Image 2 of 3

Image 3 of 3

Image 3 of 3

Faster, well-founded analyses for pitch and execution

Deeper insights (e.g., supply-chain risks, market modeling) that are often not covered internally

Competitive advantage over other advisors

Higher deal quality and a stronger negotiating position

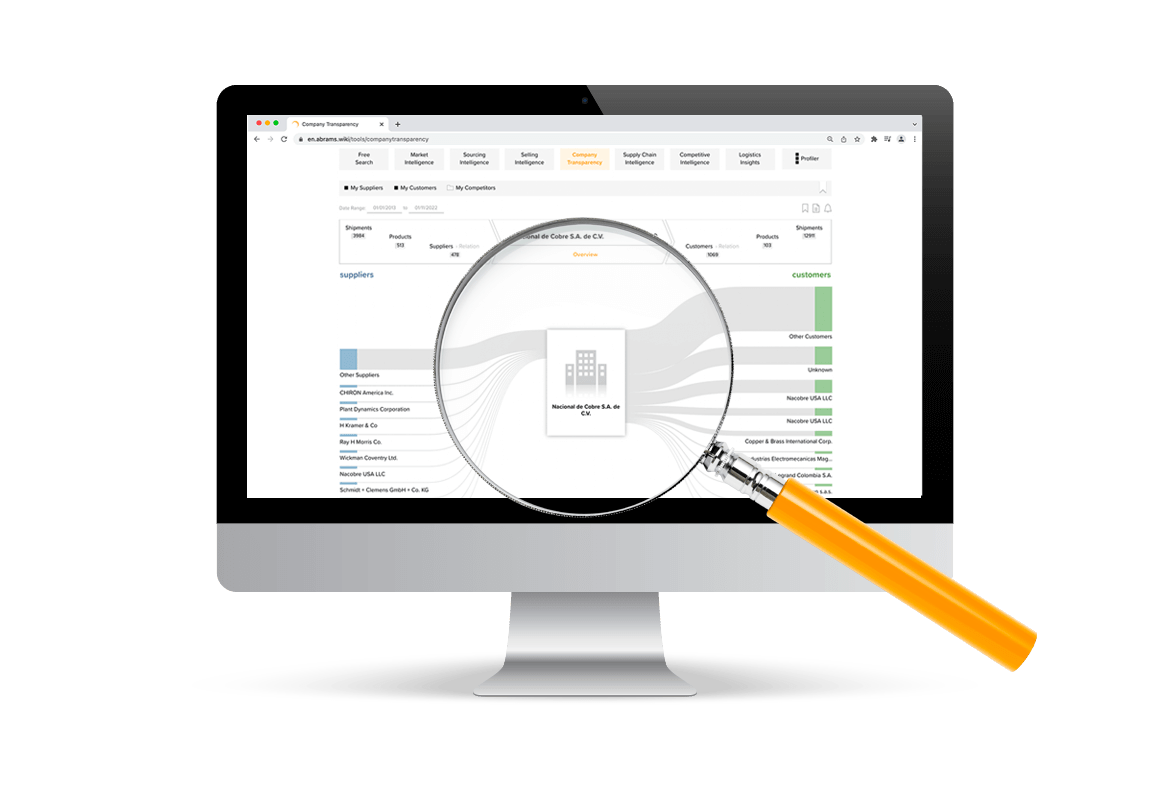

Expand breadth via the supply‑chain view — not just the “visible” firms (large, public, registered) but also critical niche suppliers or specialized customers.

Cluster by role in the value chain — tier‑1, tier‑2, bottleneck, innovation supplier.

Quickly surface hidden champions — e.g., firms with little financial visibility that are key suppliers to industry leaders.

Regional additions — trade‑flow visibility reveals alternative targets across regions (e.g., reshoring options).

Value: the longlist becomes substantially broader and more strategic by factoring in operational relevance.

Faster, well-founded analyses for pitch and execution

Deeper insights (e.g., supply-chain risks, market modeling) that are often not covered internally

Competitive advantage over other advisors

Higher deal quality and a stronger negotiating position

Expand breadth via the supply‑chain view — not just the “visible” firms (large, public, registered) but also critical niche suppliers or specialized customers.

Cluster by role in the value chain — tier‑1, tier‑2, bottleneck, innovation supplier.

Quickly surface hidden champions — e.g., firms with little financial visibility that are key suppliers to industry leaders.

Regional additions — trade‑flow visibility reveals alternative targets across regions (e.g., reshoring options).

Value: the longlist becomes substantially broader and more strategic by factoring in operational relevance.